[unable to retrieve full-text content]

What really counts? How the patriarchy of economics finally tore me apart The GuardianWhat really counts? How the patriarchy of economics finally tore me apart - The Guardian

Read More

[unable to retrieve full-text content]

What really counts? How the patriarchy of economics finally tore me apart The Guardian

Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

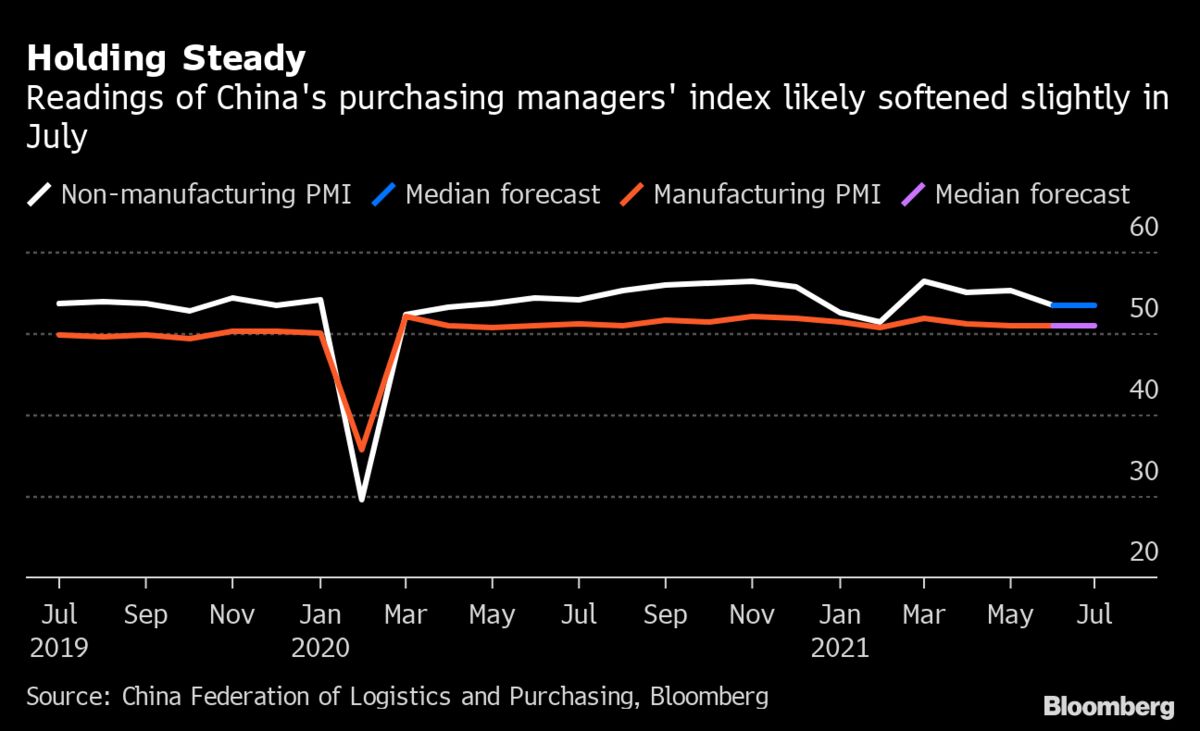

China’s economic activity continued to ease in July, implying a more steady recovery into the second half of the year as growth risks mount.

On Thursday, the White House issued an impromptu, last-minute call for Congress to extend an expiring moratorium on evictions nationwide, citing the renewed threat of the delta variant. That effort was not expected to pass and its late arrival frustrated liberal lawmakers and advocates close to the administration. Even some White House officials were confused by the sudden statement from White House press secretary Jen Psaki, which appeared incompatible with the congressional schedule. The moratorium ends Sunday, leaving lawmakers virtually no time to meet Psaki’s request.

“Why are we doing this now? Why did we wait so long? It’s very weird,” one senior administration official told The Washington Post, speaking on the condition of anonymity to reflect the mood among many officials.

The whiplash over the eviction moratorium underscores the broader uncertainty facing the administration as it tries to head off the delta variant as the other parts of its economic agenda proceed.

Even within 24 hours, the administration received deeply conflicting signs about the progress of its efforts.

On Wednesday, the White House and Senate Republicans announced they had secured a breakthrough agreement on a $1 trillion bipartisan infrastructure package, a key priority of the president’s. Thursday morning, the Department of Labor reported weekly unemployment claims had stayed relatively flat in a troubling sign of the economic rebound. Government data released Thursday also showed surging growth, with the economy growing by 6.5 percent in the quarter ending in June, while closing the gap created by the pandemic.

The eviction moratorium expiring Sunday highlighted the challenges of adjusting to the delta variant on such a rapid timeline.

The White House official in charge of implementing the stimulus, Gene Sperling, raised the idea in internal conversations over the past week of whether the moratorium could be extended unilaterally, two people familiar with the matter said. White House Domestic Policy Council Director Susan Rice and National Economic Council Director Brian Deese were also involved in discussions about extending it and supportive of the effort, the people said.

However, their suggestion ran into opposition from the White House Office of Legal Counsel, among other administration attorneys, who cited a Supreme Court opinion last month, the two people said. In voting with the court’s liberals to allow the moratorium to remain in place through July, Supreme Court Justice Brett M. Kavanaugh said that extending the moratorium further would require congressional approval.

Biden administration attorneys expressed concern that if the White House defied Kavanaugh, the Supreme Court could move to restrict other emergency public health rules instituted by the federal government, the people said. The people spoke on the condition of anonymity to discuss internal dynamics.

“There was a real desire to go back and kick the tires and say, ‘Are we absolutely sure we can’t extend?’ Everybody wanted to as a policy matter. But what was clear from the legal analysis was that we had already litigated this issue all the way to the Supreme Court, and the court had spoken on the issue,” Sperling told The Washington Post. “There was no chance of winning or it even having a temporary positive impact and some chance that it could provoke a harmful ruling.”

Still, Sperling’s explanation leaves unclear why the White House waited a month — between Kavanaugh’s June 29 opinion and Psaki’s statement on Thursday — to push for congressional action. The delay complicated legislative efforts to keep the ban in place. Two House Democrats involved in the push for extending the moratorium, who spoke on the condition of anonymity to discuss internal matters, said they had been waiting for guidance from the administration, before trying to push the effort through Congress.

The statement also said Biden would have “strongly supported” an extension in the eviction moratorium amid the delta variant were it not for the Supreme Court’s announcement. A White House statement stressed that the landscape of covid-19 had shifted rapidly since the time of the court’s ruling. The statement also emphasized the administration’s efforts to accelerate disbursal of rental assistance relief across the country.

The White House has cited strong economic growth and falling unemployment, and said it has always maintained the war against covid had not been fully won. A White House statement pointed to new efforts over the past several months to improve the pace of vaccinations and said the economy would receive further support from parts of the $1.9 trillion stimulus yet to be allocated.

Other advocates maintained the administration should have moved more quickly on the eviction moratorium. An analysis circulating among congressional Democratic offices found that millions of renters are at risk of eviction precisely in the areas where the delta variant is most strongly circulating.

“The ruling the Supreme Court gave was based on arguments filed in early June, when delta made up about 10 percent of cases. Now, delta is about 90 percent of cases and everything is surging,” said Paul Williams, a housing expert and fellow at the nonprofit Jain Family Institute and the author of the analysis.

“Why not instruct the CDC to extend it and let this go through the courts? Every day the rental assistance program can send out money and extinguish debt is evictions prevented.”

Some housing experts agreed with the White House, saying they believed that the administration’s hands were tied by the Supreme Court.

“The delta variant changed everything and created new urgency for an extension,” said Diane Yentel, president and CEO of the National Low Income Housing Coalition. “But the Supreme Court was really clear that if they attempted to extend the moratorium they would overturn it.”

Other analysts said the criticism of the administration is overblown. The economy is still set to grow at a rapid pace and much of the country is vaccinated. It remains far from clear whether the delta variant remains a long-term threat — even if that possibility continues to be a top concern of administration officials themselves.

“I think this is being overplayed,” said Dean Baker, a liberal economist. Baker pointed to a sharp decline in cases in the United Kingdom after an initial surge as a reason to be heartened. “The reality is they did a very good job getting the vaccines out.”

Still, other challenges loom. The White House has been consumed this month with pushing Congress to approve the infrastructure package and a separate $3.5 trillion spending bill. But even though the labor market remains far from fully healed, federal unemployment benefits for roughly 9.2 million Americans stand to expire in full in September, according to a recent analysis by the Century Foundation, a think tank.

Biden has been clear that he believes it is time for the additional federal $300 per week supplement to end. But another 5.2 million gig workers and other self-employed Americans are set to lose their unemployment altogether given that a special pandemic unemployment program will expire in September. Another approximately 4 million Americans are also at risk of losing long-term federal unemployment benefits.

A White House statement said the administration was still evaluating new data and pushing Congress to implement long-term reforms of the unemployment system. The White House has not answered questions about whether it will seek to extend the jobless program for gig workers and the long-term unemployed. One senior administration official said White House officials believe there is no political will on Capitol Hill for extending those benefits.

Despair in American society is a barrier to reviving our labor markets and productivity, jeopardizing our well-being, health, longevity, families, and communities—and even our national security. The COVID-19 pandemic was a fundamental shock, exacerbating an already a growing problem of despair.

This despair in part results from the decline of the white working class. It contributes to our decreasing geographic mobility and has political spillovers, such as the recent increase in far-right radicalization. At the same time, other population groups are also suffering, for different reasons. Over past few years, for instance, suicides increased among minority youth and overdoses increased among Black urban males (starting from a lower level than whites but now exceeding it).

Policy responses have been fragmented, with much focus on interdiction or ex-post treatment rather than on the root causes of despair. There are local efforts to boost the well-being of vulnerable cohorts, but most are isolated silos. There is no federal level entity to provide the vulnerable with financial or logistical support, nor is there a system that can disseminate relevant information to other communities seeking solutions. While federal agencies—such as the Centers for Disease Control (CDC)—track mortality trends, no system tracks the underlying causes of these deaths. In contrast, many countries, such as the U.K. and New Zealand, track trends in well-being and ill-being as part of their routine national statistics collection and have key leadership positions focused exclusively on these issues.

This policy paper proposes a new federal interagency task force to address our nation’s crisis of despair as a critical first step to sustainable economic recovery. The task force would both monitor trends and coordinate federal and local efforts in this arena. We identify five key areas the task force could monitor and help coordinate: data collection; changing the public narrative; addressing community-wide despair as part of the future of work; private-public sector partnerships; and despair as a national security issue.

The lead economics expert in the Federal Trade Commission’s antitrust suit against Facebook has parted ways with the agency, two individuals familiar with the case said — adding yet another impediment to the regulator’s largest court fight.

The FTC is now looking for a new expert, just three weeks before the agency must decide whether to file the new version of the Facebook lawsuit after a D.C.-based judge threw it out last month.

The expert, University of California-Berkeley economist Carl Shapiro, didn’t respond to multiple phone calls and an email asking the reasons for his departure. But he has criticized new FTC Chair Lina Khan’s aggressive approach to antitrust enforcement, and she in turn has faulted the agency’s traditional reliance on economists’ analyses in its fights against alleged monopolists.

The agency hired Shapiro, a former Obama-era antitrust official, to aid in its suit against Facebook in 2019. It has already paid out $5.7 million to the economics consulting firm where he is a senior consultant, according to a POLITICO analysis of federal contracting data. That is nearly double what the FTC has paid for any other expert services over the past two years at a time the agency has told Congress it is strapped for cash.

While the FTC retains any work Shapiro and his associates have completed, experts said much of the work will need to be redone by any new economic team hired by the agency in order to adequately defend it in court.

That’s on top of a growing pile of headaches for the FTC as it attempts to press its case against Facebook and pursues an antitrust probe of Amazon — both of which rank among the five most valuable U.S. companies. The two tech giants have demanded that Khan recuse herself from their cases, prompting an internal debate on how the FTC should respond, and she faces attacks from GOP lawmakers who accuse her of sidelining the agency’s two Republican commissioners.

The agency declined to comment on Shapiro’s departure.

“The FTC does not comment on internal deliberations over any particular expert engagement,” spokesperson Lindsay Kryzak told POLITICO. “But the agency routinely reviews its expert support needs, including to ensure that the agency is making the best use of limited public funds while carrying out its law enforcement obligations.”

The agency sued Facebook in December, alleging the company monopolized the social networking market by buying up Instagram and WhatsApp and cutting off data access to other potential rivals. A federal judge threw out the FTC’s complaint last month, finding prosecutors didn’t show Facebook controls more than 60 percent of the market. The agency has until Aug. 19 to file a new complaint.

The FTC has also been seeking a replacement for Shapiro, the top antitrust economist at the Justice Department in both the Obama and Clinton administrations and a well-known figure in antitrust litigation. He has served as the testifying expert in six FTC or DOJ cases over the past eight years, including the Trump-era Justice Department’s failed bid to stop AT&T’s merger with Time Warner and an unsuccessful attempt by state attorneys general to block Sprint and T-Mobile from merging. He also consults for Google.

Kryzak, the FTC spokeswoman, declined to comment on how much the agency has spent on expert witnesses.

The agency has pleaded with Congress for more money, arguing that its $331 million budget isn’t sufficient for its burgeoning workload of policing mergers, business conduct, consumer privacy and data security. In financial reports, the agency has cited ballooning expert witness costs as among its “top risks.”

The individuals who spoke to POLITICO didn’t know the reason for Shapiro’s exit and whether it related to disagreements about the future of the case, the costs or the history of ideological differences between Shapiro and Khan. The individuals requested anonymity to speak about internal agency deliberations.

Shapiro has been critical of Khan’s approach to antitrust, particularly her view that enforcers focus too heavily on a so-called consumer welfare standard that emphasizes price as the main sign of a lack of competition. (Critics of the tech industry say the standard is ill-suited to handling companies like Facebook and Google that offer their main products free of charge to consumers.)

In a conversation with reporters on June 28, Khan said previous antitrust enforcers relied too heavily on economic analysis to make their cases. She cited the states’ challenge to the Sprint-T-Mobile merger — in which Shapiro testified on behalf of the attorneys general — where the judge said the dueling economic experts “essentially cancel each other out” and required him to tell the future from “competing crystal balls.”

“Antitrust over the last few decades has become dependent on a particular type of economic theory,” Khan said. “The antitrust statutes are quite sparse. They are very general. There’s nothing in there about what econometric analysis to use. There’s been choices about what types of analysis to privilege.”

Two other individuals familiar with the agency’s Facebook case defended the amount of money the FTC has spent so far, noting that monopolization cases like the one against the social network are notoriously expensive. It also isn’t unusual for a new chair to seek to replace top staffers or experts in high-profile cases to better align with their priorities, one of the people said. Both spoke anonymously to discuss internal agency dynamics.

In a 2019 audit, the FTC’s inspector general found the agency pays about $750 per hour for experts and that cases involving company business conduct — like the antitrust suit against Facebook — are among the most expensive. Of the 15 contracts the inspector general audited, conduct cases accounted for $6 million of the $20 million spent.

The investigators recommended the FTC seek to use its in-house economists as expert witnesses in more cases.

Facebook, meanwhile, has the resources to put up a hefty court fight. It reported $29 billion in revenue in the most recent quarter and has a market value of about $1 trillion.

The FTC denied a public records request from POLITICO in February seeking information on expert witness contracts related to the Facebook case, saying its disclosure would interfere with the agency’s litigation. But using public data that the FTC reported to a federal government contracting database, POLITICO was able to identify the expert witness contract related to Facebook.

In the fiscal year that ended on Sept. 30, the FTC spent $21.3 million for expert witness services. So far this fiscal year, the FTC has already spent $25 million, according to federal government contracting records. The amounts paid vary between a few thousand dollars and several million depending on the work required. The $5.7 million contract is by far the largest, nearly double the amount of any other contract the agency has paid for expert witness services.

“The quantity of information both data and documents that experts have to review, use and assimilate has grown astronomically over time and that has caused expert costs to rise,” said Bruce Hoffman, who served as the FTC’s top competition staffer from 2017 through 2019.

The FTC does some of the work in-house but doesn’t have the computing power or infrastructure needed to take on all of it, said Hoffman, now a partner at the law firm Cleary Gottlieb.

Most of the expenses are probably not from Shapiro himself — who offers the government a discount on the rate he charges to corporate clients — but from the Charles River Associates colleagues assisting him. The individuals assisting Shapiro standardize data provided by companies in the investigation and do the economic calculations Shapiro requests. CRA bills the agency for the hours worked by Shapiro and its employees.

The contract terms between a consulting firm and its experts vary, but Shapiro would be paid for the time he worked plus a percentage of his assistants’ total billings, probably somewhere between 10 and 25 percent, according to two economic consultants who asked to speak anonymously to discuss what both the agency and the consulting firms consider confidential billing practices.

Both consultants said they were surprised at the amount the FTC had spent so far given that the Facebook case is just beginning. The most expensive part of antitrust litigation usually takes place later in a case, when experts prepare written reports that can run into the hundreds of pages. Those expert witness reports, which are filed in court, can cost between $1 million and $2 million to prepare, they said.

While any new expert the FTC hires could reuse the data that Shapiro and his team compiled, the consultants said, that person would insist on redoing the economic analysis to be able to defend it in court.

But Hoffman, who left the agency before the Facebook case was really underway, said he wasn’t surprised by the expense.

“It’s a complicated case. I could imagine there’s mind bogglingly large quantities of data,” he said. “There’s a little bit of irony that people all over the country are screaming that the FTC should be more active and on the other hand concerned it’s spending too much money. If you want the FTC to be active, you have to give them the money to do that.”

Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

China’s factory conditions likely stabilized in July, implying a more steady recovery in the economy in the second half of the year as growth risks mount.

AT THE START of the century, developing economies were a source of unbounded optimism and fierce ambition. Today South Africa is reeling from an insurrection, Colombia has suffered violent protests and Tunisia faces a constitutional crisis. Illiberal government is in fashion. Peru has just sworn in a Marxist as its president and independent institutions are under attack in Brazil, India and Mexico.

This wave of unrest and authoritarianism partly reflects covid-19, which has exposed and exploited vulnerabilities, from rotten bureaucracies to frayed social safety-nets. And as we explain this week, the despair and chaos threaten to exacerbate a profound economic problem: many poor and middle-income countries are losing the knack of catching up with the richest ones.

Our excess-mortality model suggests that 8m-16m people have died in the pandemic. The central estimate is 14m. The developing world is vulnerable to the virus, especially lower-middle-income countries where remote working is rare and plenty of people are fat and old. If you strip out China, non-rich countries have 68% of the world’s population but 87% of its deaths. Only 5% of those aged over 12 are fully vaccinated.

Alongside the human cost is an economic bill, since emerging markets have less room to spend their way out of trouble. Medium-term GDP forecasts for all emerging economies are in aggregate 5% lower than before the virus struck. People are angry and, even though protesting during a pandemic is risky, violent demonstrations around the world are more common than at any time since 2008.

Rich places, such as America and Britain, are no strangers to incompetence and turmoil. But disappointment has hit emerging economies especially hard. In the early 2000s they buzzed with talk of “catch-up”: the idea that poorer countries could prosper by absorbing foreign technology, investing in manufacturing and opening up their economies to trade, as a handful of East Asian tiger economies had done a generation earlier. Wall Street coined the term BRICs to celebrate Brazil, Russia, India and China—the world economy’s new superstars.

For a while, catch-up worked. The proportion of countries where the level of economic output per head was growing faster than in America rose from 34% in the 1980s to 82% in the 2000s. The implications were momentous. Poverty fell. Multinational companies pivoted away from the boring old West. In geopolitics catch-up promised a new multipolar world in which power was more evenly distributed.

This golden age now looks as if it has come to a premature end. In the 2010s the share of countries catching up fell to 59%. China has defied many doomsayers and there have been quieter Asian success stories such as Vietnam, the Philippines and Malaysia. But Brazil and Russia have let down the BRICs and, as a whole, Latin America, the Middle East and sub-Saharan Africa are falling further behind the rich world. Even emerging Asia is catching up more slowly than it was.

Bad luck has played a part. The commodity boom of the 2000s fizzled out, global trade stagnated after the financial crisis and bouts of exchange-rate turbulence caused turmoil. But so has complacency as countries have come to think that fast growth was preordained. In many places basic services such as education and health care have been neglected. Crippling problems have been left unfixed, including South Africa’s idle power plants, India’s rotten banks and Russia’s corruption. Instead of defending liberal institutions, such as central banks and the courts, politicians have used them for their own gain.

What happens next? One risk is an emerging-market economic crisis as interest rates in America rise. Fortunately most emerging economies are less brittle than they were, because they have floating exchange rates and rely less on foreign-currency debt. Long-running political crises are a bigger worry. Research suggests that protests suppress the economy, which leads to further discontent—and that the effect is more marked in emerging markets.

Even if emerging economies avoid chaos, the legacy of covid-19 and rising protectionism could condemn them to a long period of slower growth. Many of their people will remain unvaccinated until well into 2022. Long-term productivity could be lowered as a result of so many children having missed school.

Trade may also become harder. China is turning inward, away from the broadly open policies that made it richer. If that continues, China will never be the vast source of consumer demand for the poor world that America has been for China in recent decades.

The West’s increasing protectionism will also limit export opportunities for foreign producers which, in any case, will be less advantageous as manufacturing becomes less labour-intensive. Unfortunately, rich countries are unlikely to make up for it by liberalising trade in services, which would open up other paths to growth. And they may fail to help exposed economies such as Bangladesh—a success story—adapt to climate change.

Faced with this grim landscape, emerging markets may themselves be tempted to abandon open trade and investment. That would be a grave error. An unforgiving global environment makes it even more important for them to stick to policies that work. Turkey’s notion that raising interest rates causes inflation has been disastrous; Venezuela’s pursuit of socialism has been ruinous; and banning foreign firms from adding customers, as India just has with Mastercard, is self-defeating. When catching up is hard, those emerging markets which stay open will have the best chance.

Some rules have changed: universal access to digital technologies is now vital, as is an adequate social safety-net. But the principles of how to get rich remain the same today as they ever were. Stay open to trade, compete in global markets and invest in infrastructure and education. Before the liberal reforms of recent decades, economies were diverging. There is time yet to avoid a return to the needless hardship of old. ■

This article appeared in the Leaders section of the print edition under the headline "Dashed hopes"

US economic growth rose slightly in the second quarter to 6.5 per cent on an annualised basis, a weaker-than-expected increase as strong consumption was partially offset by lagging property investments and inventory drawdowns.

The data from the US commerce department on Thursday fell short of economists’ forecasts of 8.5 per cent growth on an annualised basis, and compared with a 6.3 per cent increase during the first quarter.

It nonetheless brought US output back above its pre-pandemic level for the first time since Covid-19 struck, and economists expect strong growth for the rest of the year.

Gross domestic product growth rose 1.6 per cent compared with the previous quarter, based on the measure used by other big economies. The weakest components of the report were residential investments and inventories, exposing the extent to which labour shortages and supply chain disruptions are slowing what is otherwise an exceptionally robust US expansion.

The resurgence of Covid in some parts of the country due to the Delta variant has raised concerns about US economic prospects in the weeks and months ahead. After a steady decline this spring, cases had only just started to rise again at the end of the second quarter.

Personal consumption was the strongest component of the GDP data, with spending increasing at an annualised rate of 11.8 per cent, compared to 11.4 per cent in the first quarter. Millions of US households received stimulus cheques between mid-March and early April, triggering a shopping burst as economic activity rebounded from the depths of the pandemic.

But private domestic investment declined 3.5 per cent in the quarter, dragged down by a drop in residential investments and business spending on structures. Otherwise, however, business investment was strong.

The data also highlighted rising inflation. The PCE price index increased 6.4 per cent, compared with an increase of 3.8 per cent in the first quarter. The core PCE index, which strips out volatile food and energy costs, increased 6.1 per cent, compared with a 2.7 per cent rise in the first quarter.

Economists were split on the strength of the US recovery in the second half of the year.

“Although Q2 numbers were disappointing in aggregate, the continued strength in private demand is very encouraging and should allow the economy to sustain strong momentum into the second half and 2022,” said Aneta Markowska, an economist at Jefferies, citing strong household balance sheets and inventory restocking. She expects growth of 7.5 per cent in the second half of the year on an annualised basis.

Others were more concerned. “The good news is that the economy has now surpassed its pre-pandemic level. But with the impact from the fiscal stimulus waning, surging prices weakening purchasing power, the Delta variant running amok in the south and the saving rate lower than we thought, we expect real GDP growth to slow to 3.5 per cent annualised in the second half of this year,” said Paul Ashworth, chief North America economist at Capital Economics.

$20

trilion

4th qtr. 2019 level

+1.6%

from

previous

quarter

15

Gross domestic product

Adjusted for inflation and

seasonality, at annual rates

10

5

’15

’16

’17

’18

’19

’20

’21

$20

trilion

4th qtr. 2019 level

+1.6%

from

previous

quarter

15

Gross domestic product

Adjusted for inflation and

seasonality, at annual rates

10

5

0

’15

’16

’17

’18

’19

’20

’21

Vaccinations and federal aid helped lift the U.S. economy out of its pandemic-induced hole this spring. The next test will be whether that momentum can continue as coronavirus cases rise, masks return and government help wanes.

Gross domestic product, the broadest measure of economic output, grew 1.6 percent in the second quarter of the year, the Commerce Department said Thursday, up from 1.5 percent in the first three months of the year. On an annualized basis, second-quarter growth was 6.5 percent.

The growth, fueled by strong consumer spending and robust business investment, brought output, adjusted for inflation, back to its prepandemic level. That is a remarkable achievement, exactly a year after the economy’s worst quarterly contraction on record. After the last recession ended in 2009, G.D.P. took two years to rebound fully.

+

15

%

2001

Cumulative percentage change

in G.D.P. from the start of the

last five recessions

1980

1990

+

10

+

5

2007

0

2020

–

5

–

10

5

quarters since

recessions began

10

15

20

+

15

%

2001

1980

Cumulative percent change in G.D.P.

from the start of the last five recessions

1990

+

10

+

5

2007

0

2020

–

5

–

10

5

quarters since

recessions began

10

15

20

But the second-quarter figure fell short of economists’ forecasts, and the recovery is far from complete. Output is significantly below where it would be had growth continued on its prepandemic path. Other economic measures remain deeply depressed, particularly for certain groups: The United States still has nearly seven million fewer jobs than before the pandemic. The unemployment rate for Black workers in June was 9.2 percent.

“The good news is this is all occurring much more rapidly than after the financial crisis,” said Diane Swonk, chief economist for the accounting firm Grant Thornton. “The bad news is the pain was much worse.”

Growth might have been stronger had it not been for supply-chain disruptions and labor challenges that made it difficult for many businesses to keep their shelves stocked and their stores staffed. Those issues, combined with a rush of consumer demand, contributed to faster inflation in the second quarter. Consumer prices rose 1.6 percent from the first quarter of the year to the second. Without adjusting for inflation, economic output rose 3.1 percent.

Now a new threat is emerging in the highly contagious Delta variant of the coronavirus, which has led to a surge in cases in much of the country. The Centers for Disease Control and Prevention recommended this week that even vaccinated people should wear masks indoors in some parts of the country, and some mayors and governors have reimposed mask mandates.

Few economists expect a return to widespread business shutdowns or stay-at-home orders. But if the resurgent virus leads to renewed caution among consumers — a reluctance to dine at restaurants, hesitation about booking a late-summer getaway — that could weaken the recovery at a crucial moment.

“The reason that is concerning is that this burst of activity around reopening has been driving the economy the past couple months,” said Michelle Meyer, head of U.S. economics at Bank of America. “Even a modest change in behavior could show up more meaningfully this time around.”

And this time, workers and businesses may have to face the pandemic without much help from the federal government. Roughly half the states have cut off enhanced unemployment benefits in recent weeks, and the programs are set to end nationally in September. The Paycheck Protection Program, which helped thousands of small businesses weather the crisis, is winding down. A federal eviction moratorium will end this week if the Biden administration doesn’t act to extend it. And there is no sign that Congress intends to pass a fourth round of direct checks to households.

Nela Richardson, chief economist for ADP, the payroll processing firm, said the second quarter may stand as a high-water mark for the recovery, when federal aid was still flowing and when vaccinations and the lifting of restrictions gave people an opportunity to spend.

“All the winds were going in one direction, which was to push the economy forward,” she said. “The more interesting question is: Where do we go from here?”

/cloudfront-us-east-2.images.arcpublishing.com/reuters/HFRF2JNI6JKVDOMPAQS34O37UU.jpg)

Guests enjoy outdoor dining in the Manhattan borough of New York City, U.S., May 23, 2021. REUTERS/Caitlin Ochs

WASHINGTON, July 29 (Reuters) - The U.S. economy likely gained steam in the second quarter, with the pace of growth probably the second fastest in 38 years, as massive government aid and vaccinations against COVID-19 fueled spending on travel-related services.

The anticipated acceleration in gross domestic product last quarter would lift the level of GDP above its peak in the fourth quarter of 2019. Even with the second quarter likely marking the peak in growth this cycle, the economic expansion was expected to remain solid for the remainder of this year.

A resurgence in COVID-19 infections, driven by the Delta variant of the coronavirus, however, poses a risk to the outlook. Higher inflation, if sustained, as well as ongoing supply chain disruptions could also slow the economy. The Commerce Department will publish its snapshot of second-quarter GDP growth on Thursday at 8:30 a.m EDT (1230 GMT).

"Consumers have plenty of income and wealth ammunition to support consumer spending, while business inventories remain lean and restocking efforts are poised to support business investment and overall GDP growth substantially in the second half of the year," said Sam Bullard, a senior economist at Wells Fargo in Charlotte, North Carolina.

The Federal Reserve on Wednesday kept its overnight benchmark interest rate near zero and left its bond-buying program unchanged. Fed Chair Jerome Powell told reporters that the pandemic's economic effects continued to diminish, but risks to the outlook remain. read more

The economy likely grew at an 8.5% annualized rate last quarter, according to a Reuters survey of economists. That would be the second-fastest GDP growth pace since the second quarter of 1983. The economy grew at a 6.4% rate in the first quarter, but that is subject to revision.

With the second-quarter estimate, the government will publish revisions to GDP data. Given that this is not a comprehensive benchmark revision, economists expect only modest changes to previously published estimates.

The National Bureau of Economic Research, the arbiter of U.S. recessions, declared last week that the pandemic downturn, which started in February 2020, ended in April 2020.

Economists expect growth of around 7% this year, which would be the strongest performance since 1984. The International Monetary Fund on Tuesday boosted its growth forecasts for the United States to 7.0% in 2021 and 4.9% in 2022, up 0.6 and 1.4 percentage points respectively, from its forecasts in April.

President Joe Biden's administration provided $1.9 trillion in pandemic relief in March, sending one-time $1,400 checks to qualified households and extending a $300 unemployment subsidy through early September. That brought the amount of government aid to nearly $6 trillion since the pandemic started in the United States in March 2020.

STRONG CONSUMER SPENDING

Nearly half of the population has been vaccinated against COVID-19, allowing Americans to travel, frequent restaurants, attend sporting events and engage in other services-related activities that were curbed early in the pandemic.

The pick-up in services likely boosted consumer spending in the second quarter, with double-digit growth anticipated in the segment that accounts for more than two-thirds of the U.S. economy. While spending on goods remained strong, the pace likely slowed from earlier in the pandemic, when Americans were cooped up at home.

Some of the slowdown in goods spending reflects shortages of motor vehicles and other appliances, whose production has been hampered by tight supplies of semiconductors across the globe. Higher prices, with inflation above the Fed's 2% target, could also be causing some to postpone purchases.

Though the fiscal boost is fading and COVID-19 cases are rising in states with lower vaccination rates, consumer spending will likely continue to grow.

"Those states also tend to be the ones most resistant to public health measures to combat the pandemic, such as mask mandates and limits on indoor activities," said Gus Faucher, chief economist at PNC Financial in Pittsburgh, Pennsylvania.

"Thus, the types of widespread restrictions on economic activity seen earlier in the pandemic, and then again in late 2020 and early 2021, are unlikely to be widely reimposed, which will greatly limit the economic fallout from the Delta variant and increasing coronavirus cases."

Households accumulated at least $2 trillion in excess savings during the pandemic. Record high stock market prices and accelerating home prices are boosting household wealth. Wages are also rising as companies compete for scarce workers.

A separate report from the Labor Department on Thursday is likely to show the labor market recovery gaining traction. According to a Reuters survey, 380,000 people likely filed new claims for unemployment benefits last week.

Initial claims rose to a two-month high in the week ended July 17, but economists blamed the jump on difficulties stripping out seasonal fluctuations from the data.

"The likely temporary rise in initial claims could partly be related to seasonal adjustment issues or a larger reduction in employment in the auto sector around the usual break in summer auto production given supply issues facing the industry," said Veronica Clark, an economist at Citigroup in New York.

The economy likely received a further boost from business investment, especially on equipment, as companies ramp up production, though spending on nonresidential structures such as mining exploration, shafts and wells probably declined for a seventh straight quarter.

Trade was likely a drag on GDP growth for a fourth straight quarter as strong demand sucked in imports. Expensive building materials and soaring house prices likely weighed on the housing market in the second quarter.

Inventories, which were sharply drawn down in the first quarter, are a wild card. Supply constraints have made it difficult for businesses to replenish stocks. An improvement is, however, expected in the second half as spending shifts further to services from goods.

Reporting by Lucia Mutikani; Editing by Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/QASP2Z2C2NKI7DNSCCQ27QWWEU.jpg)

WASHINGTON, July 28 (Reuters) - The U.S. economic recovery is still on track despite a rise in coronavirus infections, the Federal Reserve said on Wednesday in a new policy statement that remained upbeat and flagged ongoing talks around the eventual withdrawal of monetary policy support.

In a news conference following the release of the statement, Fed Chair Jerome Powell said the U.S. job market still had "some ground to cover" before it would be time to pull back from the economic support the U.S. central bank put in place in the spring of 2020 to battle the coronavirus pandemic's economic shocks.

"I would want to see some strong job numbers" in the coming months before reducing the $120 billion in monthly bond purchases the Fed continues to make, he told reporters.

But Powell also downplayed, at least for now, the risk that the renewed spread of the coronavirus through its more infectious Delta variant will put the recovery at risk or throw the Fed off track as it plans an exit from crisis-era policies.

"It will have significant health consequences" in the areas of the country where outbreaks are intensifying, Powell said. Yet in the prior waves of coronavirus infections "there has tended to be less in the way of economic implications ... It is not an unreasonable expectation" that would remain the case this time, he added.

"It seems like we have learned to handle this," with progressively less economic disruption, Powell said, even as he acknowledged a fresh outbreak might to some degree slow the return of workers to the labor market or disrupt planned school reopenings in the fall.

The Fed's policy statement, issued after the end of a two-day policy meeting, reflected that confidence as the central bank continues debating how to wind down its bond purchases.

There appeared to be progress in that discussion, though no clear timetable for reducing the bond purchases. Powell said there was "very little support" for cutting the $40 billion in monthly purchases of mortgage-backed securities "earlier" than the $80 billion in Treasuries, and that once the process begins "we will taper them at the same time."

Overall, however, the Fed seemed unfazed by spread of the Delta variant, even though new daily coronavirus infections have roughly quadrupled since the Fed's June 15-16 policy meeting.

"With progress on vaccinations and strong policy support, indicators of economic activity and employment have continued to strengthen," the central bank said in its statement.

The Federal Reserve building is pictured in Washington, DC, U.S., August 22, 2018. REUTERS/Chris Wattie/File Photo

Though vaccinations have slowed - and Powell plugged inoculation as the best chance to get the economy durably back to normal - the Fed said it still expected vaccinations to "reduce the effect of the public health crisis on the economy."

That should translate into strong job growth, Powell said, and eventually allow the Fed to move away from its crisis-era programs.

In December, the Fed said it would not change its asset-buying program until there had been "substantial further progress" in repairing a labor market that was then 10 million jobs short of where it was before the pandemic.

That number is now below 7 million, and the Fed for the first time acknowledged the economy had taken a step towards its benchmark for trimming the purchases.

"The economy has made progress, and the (Federal Open Market) Committee will continue to assess progress in coming meetings," the Fed said in language pointing towards a possible reduction in bond purchases later this year or early in 2022.

The Fed also said that higher inflation remained the result of "transitory factors," and was not an imminent risk to the economy or the Fed's policy plans.

'MORE UPBEAT'

Along with leaving its bond-buying program unchanged, the central bank on Wednesday kept its overnight benchmark interest rate near zero.

Karim Basta, chief economist at III Capital Management, said the "incrementally more upbeat" policy statement opened the door to a September bond taper announcement if job growth comes in strong and the coronavirus caseload does not dent spending.

Acknowledging some progress towards their goals "seems designed to give them the option to announce" as soon as September their plans for winding down the bond purchases, he wrote.

The S&P 500 (.SPX) index, which was modestly lower before the release of the policy statement, ended the session flat. Yields on U.S. Treasuries fell in choppy trading, while the dollar (.DXY) was slightly weaker against a basket of currencies.

Reporting by Howard Schneider and Jonnell Marte Editing by Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

Just when we thought we were almost done, Covid-19 cases are surging. The world may have one of the most effective vaccines ever developed, but not everyone is taking it and so we remain susceptible to the delta variant. Not surprisingly, this has renewed calls to bring back a response that makes some feel safe and under control: mask mandates. And not just for the unvaccinated; Los Angeles, St. Louis and Savannah, Georgia, are again requiring everyone to wear masks indoors. And the Centers for Disease Control and Prevention is toughening its mask guidance, too, which will provide cover for other local governments to issue mandates.

This is a mistake. The existence of the vaccine means we’re facing a different risk problem than we did a year ago, or even several months ago. Normally, governments leave most risk-taking decisions to individuals. But the nature of a novel pandemic means we don’t know the extent of what we were facing, and one person’s risk calculation will affect others. Before we had a vaccine, this uncertainty justified extreme policies such as shutdowns and mask mandates to prevent every infection we could.

Public policy responses to the COVID-19 pandemic have caused enormous global economic disruption, as have reactions from consumers and corporations. The economic turmoil is visible everywhere – in supply chains, in unemployment numbers and in housing markets.

Our panel, including Michael Ettlinger, Founding Director University of New Hampshire Carsey School of Public Policy; Kristen Broady, Metropolitan Policy Fellow at the Brookings Institute, and Jacob Faber, Associate Professor of Sociology and Public Service at New York University will discuss these trends and consider how economic disruptions will further impact our behaviors or change the fundamentals of how markets function. They'll consider the treatment of vulnerable groups and think about things like the care economy and public health infrastructure going forward.

Politics in the Era of Global Pandemic— 2.0, is produced by Ford Hall Forum at Suffolk University, the Political Science & Legal Studies department at Suffolk University, and the GBH Forum Network. Guest speakers examine the issues at play in year two of the COVID-19 pandemic, from global infection rates to the havoc on the economy, our politics, and our trust in our governments.

This virtual event will begin at 6pm Eastern Standard Time.

Forum Network events are free and available to the public, but you must register for webinar access.

GBH encourages you to use Zoom Webinar to watch for this event. Zoom is free to the public but you will need to download it to your computer first. You can download Zoom here. If you already have Zoom, you will not need to download the platform again.